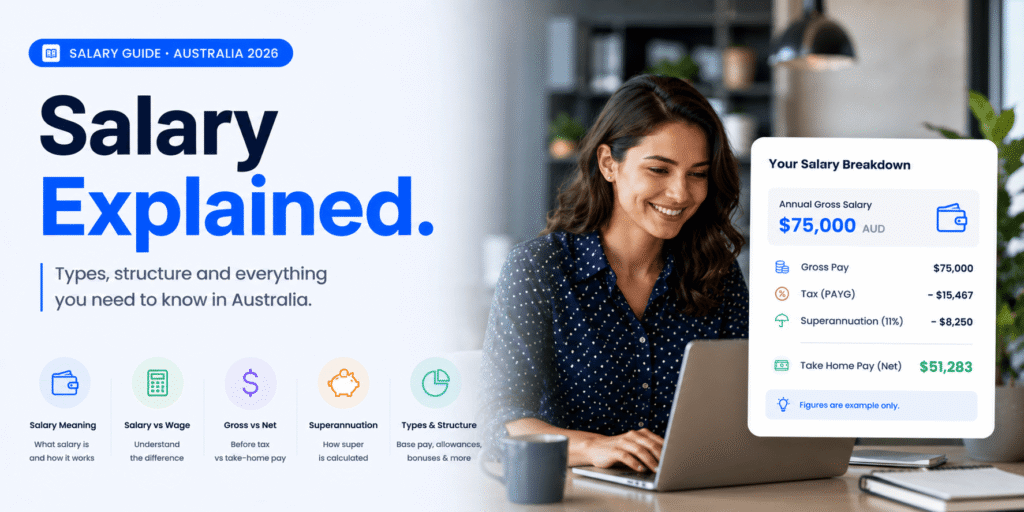

The number on your offer letter is your employer’s cost. The number that lands in your bank account is your salary. In Australia in 2026, those two figures sit further apart than most people expect, and the gap between them is not random. On $80,000 gross you take home $63,612. On $100,000 gross you take home $77,212. Every dollar that disappears between the offer and the account has a name, a legal basis and a calculation you can verify. Most Australians discover this gap on their first payslip, after they have already signed. This guide teaches you to calculate take home salary before you accept, negotiate or compare anything, so you negotiate from real numbers, not headlines. To run your figures instantly, the CloudColleague salary calculator uses ATO-verified rates for 2025-26.

| Use your salary insights to plan your next move. Start as a Seeker and discover new opportunities today. |

What is take-home salary and why it differs from gross?

Take-home salary is the net you receive after all mandatory deductions. When you calculate take home salary correctly, you know what an offer actually delivers to your account, not just what it says on paper. Gross salary is what you and your employer agreed to in your contract. The difference between them is not optional, not negotiable and not an error on your payslip.

Three things create the gap for most Australian workers who calculate take home salary in 2026. The first is PAYG income tax, where your employer withholds tax on behalf of the ATO each pay period using the current bracket rates. The second is the Medicare levy, a 2% contribution to the public health system that applies to most residents earning above the low-income threshold. The third is HECS or HELP repayments if your income exceeds $67,000 and you carry a study debt. Together, these three deductions routinely reduce a $90,000 gross salary to approximately $70,412 in hand.

What makes the gap different from person to person, even on identical gross salaries, is the interaction of individual circumstances. A worker with a HECS debt takes home less than one without. A worker who salary sacrifices $10,000 to super reduces their taxable income and keeps more of what is left. A non-resident pays tax from the first dollar with no tax-free threshold. Understanding your specific situation is what allows you to calculate take home salary accurately, rather than relying on a generic estimate that may be wrong by thousands of dollars. For how the full salary package fits together, including super and allowances, see our salary structure guide.

How to calculate take home salary: every deduction explained?

To calculate take home salary in Australia, follow a consistent sequence. Apply each deduction in order and your result matches what will appear on your payslip. Apply each deduction in order and your result matches what will appear on your payslip. Here is what each line means and how it is calculated.

Income tax using the ATO 2025-26 brackets. Australia taxes income progressively, meaning each bracket rate applies only to the income within that band. The 2025-26 resident rates, incorporating the Stage 3 tax cuts confirmed from 1 July 2024, are: $0 to $18,200 at 0%; $18,201 to $45,000 at 16%; $45,001 to $135,000 at 30%; $135,001 to $190,000 at 37%; and $190,001 and above at 45%. A $90,000 salary produces $0 on the first $18,200, $4,288 on the next $26,800 at 16%, and $13,500 on the next $45,000 at 30%. Total income tax: $17,788.

The Medicare levy. Most Australian residents pay 2% of taxable income as the Medicare levy. On $90,000 that is $1,800. Low-income earners pay a reduced levy or none, depending on their income and family circumstances. Higher-income earners without appropriate private hospital cover pay the Medicare Levy Surcharge of 1% to 1.5% on top, with the 2025-26 threshold sitting at $101,000 for singles.

The Low Income Tax Offset. The LITO reduces income tax for lower earners. The maximum is $700 and it phases to zero at $66,667. At $50,000 the LITO saves approximately $250 in tax. At $80,000 and above it saves nothing because it has fully phased out.

HECS and HELP repayments. If you carry a study debt and earn above $67,000, the ATO requires compulsory repayments via PAYG withholding. From 1 July 2025, these use a marginal repayment system where rates apply only to income above each threshold, not to your entire income. A 20% reduction was also applied to all outstanding HELP debts in June 2025. Check the ATO’s HECS repayment calculator for the rate that applies to your specific income level.

Calculate take home salary: 10 worked examples

The table below shows what you take home at ten gross income levels when you calculate take home salary using ATO 2025-26 bracket calculations. using ATO 2025-26 bracket calculations. All figures assume an Australian resident with no HECS debt and no salary sacrifice. LITO is included where applicable. The effective rate is total deductions divided by gross salary.

| Gross salary | Income tax | Medicare levy | Take-home | Effective rate |

| $40,000 | $2,913 | $800 | $36,287 | 9.3% |

| $50,000 | $5,538 | $1,000 | $43,462 | 13.1% |

| $60,000 | $8,688 | $1,200 | $50,112 | 16.5% |

| $70,000 | $11,788 | $1,400 | $56,812 | 18.8% |

| $80,000 | $14,788 | $1,600 | $63,612 | 20.5% |

| $90,000 | $17,788 | $1,800 | $70,412 | 21.8% |

| $100,000 | $20,788 | $2,000 | $77,212 | 22.8% |

| $120,000 | $26,788 | $2,400 | $90,812 | 24.3% |

| $150,000 | $36,838 | $3,000 | $110,162 | 26.6% |

| $180,000 | $47,938 | $3,600 | $128,462 | 28.6% |

All figures use ATO 2025-26 Stage 3 bracket rates. These are the same rates you need when you calculate take home salary for any gross income in the 2025-26 financial year. LITO is included for salaries below $66,667. The $80,000 and $100,000 take-home figures are confirmed by multiple ATO-based tax calculators updated in May and June 2026. Add HECS repayments and any Medicare Levy Surcharge separately if applicable.

Want the complete table from $40,000 to $200,000? Download the free CloudColleague 2026 Take-Home Salary Comparison Table. It covers every $10,000 increment and shows the HECS impact alongside each figure.

Compare your take-home to what CloudColleague’s live roles pay. CloudColleague’s salary insights hub shows verified benchmarks for your role and city so you know whether the market pays more than your current gross.

Read Next: Australian Salary Calculator 2026: Calculate Your Take-Home Pay

How salary sacrifice changes your take-home salary calculation?

Salary sacrifice is one of the few legal strategies that changes the result when you calculate take home salary. It works because sacrificing to super reduces taxable income, not just gross pay. than your gross pay rate would normally produce. By redirecting part of your pre-tax salary into superannuation or other approved benefits, you reduce your taxable income and therefore your income tax.

A verified example using ATO 2025-26 rates: on a $95,000 salary, contributing $10,000 to super via salary sacrifice reduces your taxable income to $85,000. The income tax saving is approximately $2,200 per year, according to ATO calculator data. This means the effective cost of the $10,000 sacrifice to your take-home pay is approximately $7,800, not $10,000. You give up less cash than you send to super, because the ATO taxes your sacrifice at 15% inside the fund rather than at your 30% marginal rate.

Salary sacrifice changes how you calculate take home salary at those brackets most effectively. It is most beneficial for workers in the 30% and 37% marginal brackets, because the gap between their marginal rate and the 15% contributions tax rate is the widest. It also reduces HECS repayment income at certain thresholds, creating a secondary benefit for borrowers. Before calculating take home salary with sacrifice, confirm your concessional contributions cap. In 2025-26 the cap is $30,000 per year, including your employer’s 12% Super Guarantee. Going above the cap removes the tax advantage and adds a surcharge.

| Wondering how much more you could earn gross to make the sacrifice numbers work even better? Browse what CloudColleague’s live roles pay for your field and experience level right now. |

How HECS and HELP affect your take-home salary calculation?

For anyone with a study debt, HECS and HELP repayments are the most overlooked factor when they calculate take home salary. They do not show up as a separate tax bracket, but they consistently reduce the net figure once income crosses $67,000. They do not appear as a separate tax bracket, but they consistently reduce the net figure on every payslip once income crosses the threshold.

From 1 July 2025, the mandatory repayment threshold increased to $67,000 per year. A 20% reduction was applied to all outstanding HELP debt in June 2025, confirmed by the ATO, reducing the outstanding balance for all borrowers and therefore the number of years required to repay. The repayment system is marginal, meaning rates apply only to income above each threshold band, not to total income.

The practical impact matters most in the $67,000 to $100,000 range, where the combination of income tax, Medicare levy and HECS repayments can reduce a $80,000 gross salary to a significantly lower take-home than the bracket-only calculation suggests. If you carry a HECS debt and want the exact impact on your take-home, the ATO’s official HECS repayment estimator or the CloudColleague salary calculator with the HECS toggle active will give you the verified figure.

Calculate take home salary for part-time and casual workers

Part-time and casual workers face additional complexity when they need to calculate take home salary, because the quoted gross rate rarely translates directly to the annual equivalent most people compare against, because the gross figure on an offer is almost never the annual equivalent most people compare it to.

For part-time employees, calculate the annual equivalent first by multiplying the hourly rate by the contracted hours per week and then by 52. A 24-hour-per-week part-time role at $30 per hour produces an annual equivalent of $37,440. Apply the ATO brackets to that annual figure to find the tax, then divide back down to a weekly, fortnightly or monthly take-home. The ATO applies tax at the rate appropriate to the annualised income, not to the actual hours worked, which is an important distinction for workers who vary their hours.

Casual employees add a 25% loading to their base rate in place of paid leave entitlements. That loading is fully taxable and is included in the gross figure for take-home calculation purposes. A $30 per hour base rate becomes $37.50 casual, with tax calculated on the annualized equivalent of the casual rate. For the full comparison between hourly and salaried structures in Australia, see our salary vs hourly pay guide. Contractors who set their own rate and invoice directly can manage their payment and super through CloudColleague’s built-in payment tools via CloudColleague platform features.

When your take-home salary calculation is wrong: tax returns?

When you calculate take home salary using a payroll tool or payslip estimate, the result is an approximation, not a final tax position. Your employer’s PAYG withholding produces a real-time deduction based on an annualised projection of your income. The two do not always match, and the difference is reconciled through your annual tax return.

If your employer withheld more tax than your actual liability across the year, the ATO refunds the difference after you lodge. This is the most common outcome for workers whose income, deductions or offsets were not fully accounted for in PAYG withholding. If your employer withheld less than your actual liability, which can happen with multiple income streams, irregular income or unreported investment income, you owe the shortfall at lodgement time.

The practical lesson is that when you calculate take home salary from your payslip, the figure shown is the PAYG withholding estimate, not your final tax position. Keeping accurate records of deductible expenses, salary sacrifice amounts and investment income throughout the year allows you to reconcile accurately and avoids surprises at tax time. When you calculate take home salary for planning purposes, treat the PAYG figure as an estimate and the tax return as the final answer. Once you understand your take-home calculation, the next step is knowing how to use it. Our salary negotiation guide shows you how to turn a clear understanding of your market rate and your take-home into a persuasive pay conversation.

| Get started in minutes. Create your free seeker account and showcase your skills. |

Calculate take home salary FAQ

Take-home salary is the net amount that reaches your bank account after the ATO deducts income tax, the Medicare levy, and any HECS repayments from your gross salary.

Apply the ATO 2025-26 progressive bracket rates to your gross salary, add the 2% Medicare levy, subtract any LITO offset, and deduct HECS repayments if applicable. Use the CloudColleague salary calculator for an instant, ATO-verified result.

Effective tax rates (income tax plus Medicare levy) range from approximately 9% at $40,000 to 28.6% at $180,000, rising progressively with income as shown in the worked-example table above.

Standard employer super does not reduce take-home pay; it sits on top of your gross salary. Voluntary salary sacrifice into super does reduce your cash take-home, but also reduces your income tax.

It depends on your income level and remaining debt balance. Repayments apply above $67,000 from 1 July 2025 using a marginal rate system. Use the ATO’s HECS repayment estimator for your specific income and balance.

Gross salary is your contractual pay before deductions. Take-home is what remains after income tax, Medicare levy and HECS repayments. The gap is typically 20 to 29% for most full-time workers in Australia.